The takeover of Altium (ALU) has been done and Slack Investor had some cash at his disposal. At the end of April 2024, he went through the Slack Process of deciding which stocks to buy with the money that Altium was about to provide. In the spirit of this great company, he concentrated mostly on growth stocks and presented the list below.

Some of the stocks that Slack Investor owns are like old friends. He is always looking to add to ‘tried and true’ stocks with a good track record of growth and good management. All of the above were considered. However, as REA was already a large holding (7.9%), Slack Investor passed on REA. He did buy some TLX and also added to his holdings of TNE, SNL, NDQ, CAR and PME.

One thing he insists on however, is that they have a pleasing income chart that shows both historical growth (Black bars) and projected growth (Grey bars) – from Marketscreener.

Income growth and projected growth for XRF Scientific – From MarketScreener – Financial tab

As well as increasing income, Slack Investor likes his stocks to be profitable – a projected ROE (in 2026) to be more than 15%. He also wants them to be not too expensive – a projected P/E ratio (in 2026) of less than 40-50. Of course, he also screens for growth, using the 3-yr CAGR – and hope that it is also above 15%.

Slack Investor is not sure how any of these stocks will fare – but if you get the numbers right, good things will happen on most occasions. The 3-yr CAGR for Nick Scali is low at 8%, but past results were affected by COVID 19. Slack Investor has bought some NCK as they have just expanded into the UK and, if anyone can make this work, it will be the crack management team at Nick Scali.

Company

Ticker

ROE 2026

P/E 2026

CAGR 3-yr

Buy Price

Price 9/10

Megaport

MP1

25

37

35

$9.03

$7.39

Nick Scali

NCK

36

13

8

$13.73

$16.13

XRF Scientific

XRF

18

20

24

$1.55

$1.70

Betashares Diversified Growth

DHHF

–

–

–

$34.01

$34.78

Botanix Pharma

BOT

27

18

–

$0.37

$0.37

Betashares NextGen NASDAQ

JNDQ

–

–

–

$15.47

$15.80

Webjet

WEB/WJL

16

22

16

$9.03

$7.89

RPM Holdings

RUL

15 (?)

39

18

$2.57

$2.86

These newer stocks are in the Slack Investor ‘nursery’ for now. Sometimes a company looks good on paper – but fails to keep growing for a number of reasons (often these reasons are opaque to Slack Investor)! While in the nursery, Slack Investor keeps a weekly watch and if they fall below the buying price by around 15%, he will usually cut his losses and sell.

This happened to Megaport (MP1). He sold the holding a few weeks ago for around $7.90. Webjet (WEB) has just gone through a stock split into WEB and WJL – and is on a close watch.

Slack Investor is off on holiday to Thailand tomorrow … and, has pushed this post out early (before his usual mid-month burst of activity).

Slack Investor tries to be a little diversified in his investing with his Three Pile Theory. Although my Investment Pile (The Slack Fund) consists mostly of Australian and International Shares, my Stable Pile (about 30% of retirement funds) consists of annuities, Real Estate ETFs, Fixed Interest products, some high dividend paying shares and some Cash. I own no bonds, Gold or Cryptocurrency. I am not very strict about rebalancing … but, that’s because I am slack! Deep down however, I’m convinced that diversification makes good financial sense.

A quick look at the yearly Vanguard diversification table below shows the percentage annual total returns for 9 different asset classes. I have only shown the last 17 years, but the 30-yr table can be found here in .pdf form.

For financial year 2024, the best performers were: Australian listed property returned 24.6%, US shares 24.1% and hedged ($AU) International shares 21.5%. The point of the Vanguard table is to highlight that it is very hard to try and predict the yearly winner. Slack Investor notes that International shares (particularly the US) have featured in the top 3 for a lot of these last 17 years. He also notes that Cash is a rare top performer – but, well done for 2022! It is always useful to have a look at the Vanguard Long Term Investing chart for a reminder of the compounding power of share investing.

Auto-Diversification

Superannuation

All of your Super contributions end up in a fund that is diversified to some extent. You usually can decide on how diversified you want it to be. For example, Australian Super offers, in their pre-mixed options: High Growth, Balanced, Socially Aware, Indexed Diversified, Conservative Balanced and Stable offerings. Even their High Growth option is split into a number of different asset classes – though their ranges seem a little ‘loose’ for full disclosure to their clients.

Slack Investor’s instincts has always been to be invested with the highest growth option … though I did reassess this a few years before retirement!

Other Investments

OK then, super is taken care of … but what if you want a diversified option for other investments that could be assured long-term growth without constant input. This is where robo advice might shine. Robo advisors usually package a mixture of low cost ETF’s into a diversified portfolio with automatic re-balancing.

Slack Investor is aware of many robo advisers that operate in Australia. ValueWalk has prepared an excellent summary article. Valuewalk compares and reviews: CommSec Pocket, Spaceship Voyager, Betashares Direct, Raiz, Sharesies, Pearler, Stockspot and InvestSMART.

There is a sliding scale management fee for which all admin and rebalancing is taken care of. For example, for account balances of $200,000+, there is an annual fee of 0.528% per year.

When Slack Investor loses the ability to stock pick growth stocks effectively (or, perish the thought … shuffles off this mortal coil!), I will set up some succession plans that will move our investments onto a secure ‘minimal involvement’ platform such as robo advice.

Slack Investor is old fashioned when it comes to ETF ownership. I much prefer the robo advisers that run under the HIN system (Holder Identification Number) – where the ETF’s are registered in your own name. This makes things simple if the robo adviser should cease operations e.g. Six Park (Aust).

The alternative is the ‘custodial’ system – where the investments are held on your behalf. Although custodial models can have lower costs – I like to see my name on the ownership documents. Stockspot is one of the advisers that run under the HIN system.

Although Slack Investor is a great believer in finding out about financial things for yourself with the magic of the internet. This way is not for everyone. Let’s just be clear, for most people, if you want specific advice on wealth management, tax advice, estate planning or a multitude of other finance problems, you are best counselled to seek a qualified financial adviser.

However, if you have a lump of money that you want invested in a diversified way that suits your risk profile, then robo advice seem a relatively cost-efficient way to ensure your investments are spread across asset classes. Naturally, Slack Investor would like the fees charged by robo advisors to come down a little before he parts with his Slack funds.

September 2024 – End of Month Update

Another month with a big range of daily closing values. The ASX 200 (+2.2%) and the S&P 500 (+2.0%) are in all time high territory. The FTSE 100 languishing and down 1.7% for the month.

Slack Investor remains IN for all markets.

The recent strength of the US market has pushed the closing monthly value to more than 15% above my old stop loss. I adjusted the stop loss upwards to a new ‘higher low’ of 5119.

Weekly chart for the S&P 500 Index showing the stop loss revised upwards to the new “higher low” of 5119.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

The quarterly updates showing the shares in the Slack Portfolio have also been completed.

Van Morrison’s 1986 album No Guru, No Method, No Teacher – One of his best. Try a meditative sample – In the Garden

Van Morrison is said to have echoed the thoughts of Jiddu Krishnamurti when naming this great album back in 1986 – after 38 years, it still stands up!

“…there is no teacher, no pupil; there is no leader; there is no guru; there is no Master, no Saviour. You yourself are the teacher and the pupil; you are the Master; you are the guru; you are the leader; you are everything.” – Jiddu Krishnamurti, Indian Philosopher (1895 – 1986)

The ultimate aim for Slack Investor readers is to fund your own retirement, but for most Australians, there is still work to do. The latest available ATO statistics (FY2021) indicate that the median superannuation balances for ages 65-69 are $213,986 (Male) and $201,233 (Female).

According to the Association of Superannuation Funds of Australia (ASFA) estimates – the minimum Superannuation balances required to achieve a comfortable retirement are set out below – and these figures rely on a couple of big assumptions. You need to own your own homeand have access to the aged pension, or part-pension, to make this sum work.

To retire independently (i.e. no government aged pension), a greater lump sum would be required! Things are slowly getting better with recent increases in compulsory superannuation. By 2050, the expected percentage of “comfortable retirees” should be 50%. This is outlook shows promise – but there is a need for more Australians to take action for themselves – Right Now!

Currently, (only) around 30 per cent of couples and singles reach or exceed the ASFA Comfortable Standard (in retirement savings) – ASFA Update – November 2023

Slack Investor would add to this wonderful guidance:

Educate Yourself in the ways of finance – The internet and financial independence books are your friend here. No-one will represent your interests better than you

Automate your savings – Into superannuation and your own investments – What you don’t see, you wont spend

Your Savings Rate is a very important number – my savings rate while working and raising a family fluctuated between 20% and 45%. Far more heroic rates are documented by F.I.R.E. enthusiasts e.g. Strong Money Australia – this will accelerate your journey

Let time be your partner in long-term investing – start as early as you can.

The Slack Investor path was more of a climb up a cobbled street than a path. It involved lots of different strategies. Trying to maximise my superannuation contributions, buying a house to live in, using home equity to gear into individual stocks and ETF’s. In the last 10 years, I have been trying to invest mostly in growth stocks, without too much trading. This has been a good fit for my temperament.

Long term Investing

The real business is to be invested at leastsomewhere in appreciating assets – and let time do its work. Below is an extract from the Vanguard 2024 long-term investing chart. The numbers on the right are the results of investing $10,000 in the Index funds of the indicated asset classes for 30 years. It is Slack Investors favourite chart.

Extract from the 2024 Vanguard Index chart (Just the 2007-2024 portion is shown) – the dollar values on the right are the results of investing $10,000 in index funds in each asset class for 30 years (since July 1994). – Check out the full 30-year glory of the Vanguard 2024.PDF chart – Click image for better resolution of this portion.

August 2024 – End of Month Update

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

The S&P 500 (+2.3) continues its enthusiastic progress. Slack Investor is pleased to go with the flow but remains nervous for the US markets.

For the ASX 200 (+0.0%) and the FTSE 100 (0.1%) – things have ended up dead flat. Although, all markets have shown a lot of variation this month.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

“… nearly all the grandest discoveries of science have been but the rewards of accurate measurement and patient long-continued labour in the minute sifting of numerical results.”

Like Lord Kelvin, Slack Investor likes to measure things. FY 2024 was another good year for share owners. In the world markets, the FTSE 100 Total Return Index was up 11.4% (last FY up 7.8%). Dividends helped the Australian Accumulation Index to be up 12.2% for the financial year (last FY +10.6%). The S&P 500 Total Return Index is again the top performer – and was up 24.2% (last FY +19.7%) for the same period. All of these Total Return Indices include any accumulated dividends.

Slack Investor has stuck to his strategy of investing with growing companies that have an established earnings record and forward P/E ratios <50 (Mostly!). I expect a bit of volatility in my (mostly “growth”) investment portfolio and I am reassured that, despite the odd negative year in the Slack Investment Portfolio , the dividends and the Stable Income portfolio are doing what they should and keeping Slack Investor with enough cash to “keep the wheels on” the Slack lifestyle.

Slack Portfolio Results FY 2024

All Performance results are before tax. The Slack Portfolio is Slack Investor’s investment portfolio and, due to some lucky stock selections (e.g. ALU and PME both doubled in value FY2024), this was my “best ever” year. I’m glad to report an annual FY 2024 performance of +39.4%. Full yearly results with Australian benchmarks are shown in the table below. However, the portfolio performance in the first 6 weeks of this new FY has brought me back to Earth. Slack Investor realises that only long term results really count.

For property values, Slack Investor is using the Total Return values supplied by CoreLogic. The Total Return is calculated from value change as well as the gross rental yield. I would have preferred calculations that include the net rental yield, but this will have to do. The Total Return is a more realistic figure when comparing real estate returns to stock market total returns, as it treats both asset classes as investments with income coming from rent/dividends.

Although it is hard to match US market growth this year (+24.2%). The Australian Share market Total Return Index (ASX200 Acc) was up 12.2%. The Vanguard Diversified Growth ETF (VDGR), comprising International shares (42%) and Australian Shares (28%), increasing by 11.4%. Inflation is again above Reserve Bank target – with the CPI at +3.8%. The readily available Cash rate of 4.0% has edged above inflation for the first time in 4 years. Cash is important but not a way to grow your investments.

Although I collect yearly figures, the 5 and 10-year compound annual performance gives me a much better idea about how things are really going. Long term results will smooth out any dud (or remarkable!) yearly figures. The Slack Fund is still ahead of most Benchmarks – but running “neck and neck” with Brisbane Residential real estate over a five-year period.

Slack Investor 5-year compound annual rate of return – compared to benchmarks – Click for better resolution.

Growth of a $10000 Investment Since 2009

The beauty of compounding with a succession of good performance results can be seen in the chart below showing the growth of an initial investment in June 2009 of $10000.

The rate of growth of $10000 invested by Slack Investor in FY 2009 – compared to benchmarks – Click for better resolution.

Slack Fund has exceeded my expectations. Also, the chart shows that investing in either shares or residential property has been a solid way of growing your money over the long term.

10-year compound annual rate of return

The Slack Fund has been around a while and, I am generating some good long term data (10-year compound “rolling” annual rate of return). Over this time frame, the Slack Fund has been performing very well. A 10-year annual rate of return of over 15% – Go Slack Fund! The 10-yr data is shown below in chart and table form.

It is useful to note that, the 10-yr rates of return of the Median Balanced Fund, Vanguard Growth fund, ASX200, and residential property in Brisbane and Melbourne are also great long term investments. These appreciating assets generate a 10-year compound annual rate of return of 6-9% p.a.

From the figures below, although Cash can add stability to a portfolio, Cash as a long term investment, is a poor choice.

The percentage yearly returns quoted in this post include costs (brokerage) but, the returns are before tax. This raw figure can then be compared with other investment returns. I use the incredibly useful Market Screener to analyze the financial data from each company and extract the predicted 2o26 Price/Earnings (PE) Ratio and Return on Equity (ROE). This excellent site allows free access (up to a daily limit) to their analyst’s data, on the financials tab for each stock, once you register with an email address.

Slack Investor Stinkers – FY 2024

Financial year 2024 was generally a “boomer”. All of Slack Investors followed markets (Australia, the UK and the US) have had a pretty solid year … especially the US! However, Slack Investor knows that stinkers are a part of the game, even in good years – and managed to attach himself to a few stinkers along the way.

Global X Battery Tech & Lithium ETF (ACDC) -15%

(ACDC –2024: PE 11, Yield 3.0%) I have owned this ETF for 3 years now – and I think I might have fallen for the “Theme Dream”. Despite some early promise in the “sexy” sector of electric cars and lithium batteries, this ETF has started to disappoint. There has been a string of bad news in the electric vehicle sector with an oversupply of vehicles. Both the EU and the US have slapped large tariffs on the Chinese EV exports – this has further slowed demand. Slack Investor is just holding on and has set a stop loss at $82. Current price is about $83, so I am very close to selling – and moving on.

Coles Group (COL) -8% (Mostly sold Nov 2023)

(COL – Forecast 2026: PE 19, ROE 32%) Coles is where I often buy my groceries and I like the idea that you can regularly inspect your holdings. However, Coles Group are profitable but not really growing. This company does not really belong in my investments pile, so I mostly sold this holding. I might buy some for my stable income pile if there is a future weakness in price.

Computershare (CPU) -5% (Sold April 2024)

(CPU– Forecast 2026: PE 16, ROE 36%) Computershare was a stinker last FY for Slack investor. In retrospect, I can’t believe Ibought in again for further punishment. I keep falling for the high ROE (36%) and relatively low PE (16) for a tech stock. Might have been a little early here in folding again – the share price has risen about 12% overall in FY2024.

Slack Investor Nuggets – FY 2024

Nuggets were everywhere this Financial Year. Slack Investor continues to invest in high Return on Equity (ROE) companies with a track record of increasing earnings. Companies with these qualities sometimes behave as “golden nuggets”.

Pro Medicus (PME) +118%

(PME – Forecast2026: PE 76, ROE 46%) Pro Medicus is a developer and supplier of healthcare imaging software and services to hospitals and diagnostic imaging groups. In 2019, Slack Investor met the CEO and co-founder of Pro Medicus, Dr Sam Hupert. I was impressed by his humility and passion for his great products. I’m obviously glad I bought in – but naturally wish I’d bought more! The very high predicted PE ratio (+76) is worrying but, in the past, product sales have just kept growing above expectations as PME expands into the US.

Altium (ALU) +106% (Sold pending takeover)

(ALU – Forecast 2026: PE 32, ROE 33%) Altium is an Australian based developer and seller of computer software for the design of electronic products worldwide. My ode to this great company expands on why I originally bought it and its great management team. Good luck with the new Japanese owners Renesas. For current holders, I think the cash payment per share is due today (1 August, 2024)

Goodman Group (GMG) +75%

(GMG – Forecast 2026: PE 23, ROE 12%) Goodman Group owns, develops, and manages (mostly industrial) properties all over the world. On a weekly bike ride, I go past a succession of Goodman warehouse properties – and they always seem to be thriving with activity. They even develop data centres that will hopefully be full of machines to manage the AI trend. Glad to be an owner.

Codan (CDA) +54%

(CDA – Forecast 2026: PE 20, ROE 21%) Codan is a technology company that specializes in communications and metal detecting. It is one of Slack investors core holdings that has taken him on what can only be described as a “journey”. A nugget in FY 2021 (+161%), a stinker in FY2022 (-58%) – and now back to a nugget (+54%). What has kept me in the stock was the low debt (generally) increasing earnings, and the high profitability (ROE 21%).

Supply Network (SNL) +54%

(SNL – Forecast 2026:PE 18, ROE 36%) Supply Network are a bus and truck parts distribution company using the Multispares brand. Although there are competitors in the big-vehicle parts business, what sets SNL apart from the rest is their great management and strict adherence to processes and efficiency. They have consistently held a profitability advantage over their rivals. They have maintained a high Return on Equity (ROE) of 36% even as the company has expanded and grown in price.

Alphabet (GOOGL:NASDAQ) +52%

(GOOGL– Forecast 2026: PE 17, ROE 25%) For more good things on this company that is everywhere. High profitability (ROE 25%) and the predicted 2026 PE of 17 makes this still a good buy at current prices – in Slack Investor’s head.

CAR Group (CAR) +52%

(CAR – Forecast 2026: PE 31, ROE 14%) Car Group is a collection of digital marketing vehicle businesses that are now in Australia, Brazil, Canada, Chile, China, Malaysia, New Zealand, South Korea, Thailand and the United States. The Australian business is still carsales.com. The ROE is slipping below 15%, but happy to hold on for now.

REA Group (REA) +39%

(REA – Forecast 2026: PE 41, ROE 32%) Like Carsales.com, REA has dominated the space left by the old newspaper classifieds in selling real estate in Australia and has continued to expand overseas. A high PE ratio (41) but while projected Return on Equity (ROE) remains high (32%), this is OK.

Wesfarmers (WES) +39%

(WES – Forecast 2026: PE 27, ROE 33%) Wesfarmers is Australia’s largest conglomerate. Great retail outfit (e.g. Bunnings) and chemical manufacturer. High profitability (ROE 33%) but like Coles, seems low on earnings growth lately.

Some honourable mentions to some top results this year that didn’t make the nuggets. BetaShares NASDAQ 100 ETF (NDQ) +32%; BetaShares Global Quality Leaders ETF) +27%; BetaShares Global Cybersecurity ETF (HACK)+26%; Dicker Data Limited (DDR.AX)+26%. A special mention also to a recent buy, Telix Pharmaceuticals (TLX) +23% in two months!

Slack Investor Total SMSF investments performance – FY 2024 July 2024 end of Month Update

Slack investor has just two piles of funds for his retirement – the Stable Income pile (Cash and Conservative) and an Investments pile. The Stable income represents just 25% of total retirement funds. I used to rebalance each of my piles after every year, but the stable pile now has enough in it that, together with dividends from my investments, could supply me with enough living expenses to last out an extended (3-yr) bad run of the stock markets – without having to sell stocks. The stable pile produces a moderate return of about 5%. The Investments pile is much more fun and the figures below represent (before tax) performance of my investmentspile only.

After a difficult 2022, a solid 2023, some very good fortune was had with a ripper FY2024. Some fortuitous selections with growth stocks have really paid off (Thank you PME and ALU). In the Australian superannuation scene, the median growth fund (61 to 80% in growth assets) returned +9.1% in FY 2024. The ASX 200 chart shows a gradual climb after a shaky start for the financial year.

A record result for Slack Investor in his growth investments portfolio. His preliminary total SMSF performance looks like coming in at around +39% for the financial year. Including the relatively low returns from my stable income pile (~5%) – overall, my retirement funds grew about 30%. A very good year!

For Slack Investor, the 5-yr performance is a more useful way of measuring – as it takes out the fluctuations of yearly returns. At the end of FY 2024, the Slack Portfolio has a compounding 5-yr annual return of around 13%.

July 2024 – end of Month Update

The new financial year has started off positively for Slack Investor markets. The ASX 200 + 4.2%; FTSE 100 +2.5%; and S&P 500 +1.1%. He remains IN for all index positions.

I have taken the opportunity to adjust upwards the stop losses on all followed index markets. The prices have crept up to more than 15% above their old stop losses. See Index pages for details.

All Index pages (ASX Index, UK Index, US Index) and charts have been updated to reflect the monthly changes.

This continues the series of judgement – on a few calls by Slack Investor in recent blogs. The good and the bad are presented – to illustrate that you don’t have to get everything right to be a successful investor.

I tried to make the case that the ASX 200 was both undervalued and showing signs of momentum in the charts. At the the publishing dates, the ASX 200 was trading at 7328 and 7267. At 30/06/24, it is 7767, up 5.9 % and 6.8%. In the meantime, the US S&P 500, which Slack Investor thought was overvalued at the time, is up 32% for the same period. Could do better, Slack Investor – 5/10

I went through a whittling down process for a few stocks that might be suitable for my nephew who was just starting out on his investing journey. I wanted to gather a basket of well known, growing companies that were not outrageously over priced- I generally don’t like the predicted P/E Ratio to get above 40 when I’m buying, as this indicates the current price of the company is 40 times its predicted earnings (expensive) . The yield (dividend) is not that important to a young investor, it is the total growth that counts.

Looking at the figures, even Slack Investor is surprised with the success of his suggestions after only 12 months – an average 1-yr growth of +34.2%.

Again, Coles Group (COL) is the only dud. Despite COL having a high Return on Equity (ROE), I should have considered the competitive retail environment, its lack of history of growth and how it was spending most of its profits – returning to shareholders as dividends, rather than growing the business.

I hope that my nephew took this advice and is now a convert to stocks as a way to make your money grow. A top effort Slack Investor9/10; Nephew?/10

I went through the Slack investor buying process and I had to narrow things down to the one new share that I would buy at the time with a limited amount of funds. I selected Computershare (CPU). In hindsight, I should have trusted my gut here – I have never liked their confusing website! At the the publishing date, CPU was trading at $25.85. At 30/06/24, it is $26.34, up 1.8%. I had sold out of this stock, at a loss, 5 months after I bought it as I didn’t like the way that the chart was heading. A dud trade Slack Investor – 1/10

Slack Investor went a bit in depth here as to why Alphabet (NASDAQ : GOOGL) was such a major portion of his portfolio. At the the publishing date, GOOGL was trading at $137.36 USD. At 30/06/24, it is $182.15 USD, up 35%, A good trade Slack Investor, is this all your own work? – 9/10.

I am delighted to report that Centrelink have sent me a Commonwealth Seniors’ Health Card (CSHC). I have yet to make use of it … but I am excited that my perseverance with the forms (with the help of very generous new annual income limit rules) has paid off. You really tried hard here Slack Investor8/10; Centrelink 3/10 – The application process is confusing and tedious. The turn around time for the application was about 2 months – but, I don’t blame the workers at Centrelink here – there has been chronic underfunding in staff and processes for years.

Financial Year 2024

A quick review of how the Slack followed markets fared in FY 2024 – pretty well I might say!

ASX 200

ASX 200 Weekly chart for FY 2024 (Click to Enlarge) – From Incredible Charts

After a solid 2023, FY 2024 could be described as a slow start – but big finish. In raw figures the Australian Index rose 7.8 %. When accumulated dividends are re-invested, the ASX 200 Net Total Return, the yearly returns are more impressive, up 12.2%.

FTSE 100

FTSE 100 Weekly chart for FY 2024 (Click to Enlarge) – From Incredible Charts

This bad boy has shown great improvement. The UK Index rose 8.4 %. When accumulated dividends are re-invested, the FTSE 100 Total Return was up 11.4%.

S&P 500

S&P 500 Weekly chart for FY 2024 (Click to Enlarge) – From Incredible Charts

That crazy country, the mighty US of A, has done it again. the US Index rose 22.7 %. When accumulated dividends are re-invested, the S&P 500 Total Return was up a mighty 24.2%.

Slack Investor does not provide specific advice, but occasionally he will expand on the way he invests and report on the things that he is looking at. I will sometimes mention actual stocks or financial products that I am interested in.

I don’t regard myself as a gun “stock picker”- my long-term success rate for “winning” stocks is about 55% for completed trades over a 20-yr period. What I think I am OK at though, is weeding out the dud trades and sticking with the winners. My overall results are good. I find that if you surround yourself with solid growing companies – more good things will happen than bad things.

I think a couple of follow up posts are in order to pass judgement on some of the good, and bad, ideas that Slack Investor has thrown out into the world.

Slack investor had a bit of loose change and was “on the buy”. I outlined my case for Alphabet (GOOGL.NASDAQ), the Betashares NASDAQ 100 ETF (NDQ.ASX), and the Coles Group (COL.ASX).

Slack Investor was looking at technology changes in the music Industry using one of the more interesting charts that he has found. Who knew that “Peak Revenues”, from cassettes was in 1980, from CD sales in 1999, and peak music downloads in 2005. The only music revenue games in town now, are streaming, and live performances.

This was a roundabout way of showing the profound effect and fast moving pace of technology. I suggested a good way to capture this technology tidal wave was Betashares NASDAQ ETF(ASX: NDQ). The share price at publishing time was $32.47, at 30/06/2024 it is $45.51, up 40.1%. Well done Slack Investor– 8/10

The human trait of innovation was explored and this was also seen to be a great attribute for companies that I would like to invest in. A simple way to expose yourself to innovation on the Australian market was through ETF’s. Betashares NASDAQ ETF(ASX: NDQ), BetaShares Asia Technology Tigers ETF (ASX: ASIA) and the ETFS Morningstar Global Technology ETF(ASX: TECH) were thought to be a way to do this.

ETF

Price 30/06/23

Price 30/06/24

% Growth

NDQ

$35.25

$45.51

+29.1%

ASIA

$9.29

$9.21

-0.6%

TECH

$101.90

$95.9

-5.8%

Average Growth

+7.6%

Some “Innovation” ETF’s

With the exception of NDQ, not so good here and it is another internal warning to avoid the over-curated themed ETF”s. I am sill investing in NDQ, but I sold out of ASIA after 9 months as China was adding some “government risk” to their stock market. Fortunately, I didn’t get around to investing in TECH. An inconsistent effort, Slack Investor seems easily distracted – 5/10

One of the Slack favourites, CSL, asked shareholders to stump up some money in a Share Purchase Plan. The asking price was $273 – which I thought was OK for such a great, growing company. The share price at 30/06/24, is $295.21, up 8.1%. A solid performance, Slack Investor, but not shooting the lights out – 6/10

I liked the look of Dicker Data (DDR) after a slump in its share price. At the the publishing date, DDR was trading at $10.44. At 30/06/24, it is $9.66, down 7.5%. Since November 2022, there has been a downgrade in profits and the CEO has sold 10% of his shares. The forecast numbers still look OK, but so far disappointing. DDR is on shaky ground – and could get the chop! Needs Improvement, Slack Investor – 2/10

Slack Investor had a “bit of a go” at famous US investor Cathie Wood and her ARK Innovation ETF (NASDAQ: ARKK). My case was, that their was a lot of talk … and not much performance from her $6 billion USD actively managed fund. The price chart has continued to languish, and her 5-yr performance figures have got worse – and well behind the performance of the passive S&P 500 and NASDAQ 100 ETF’s. The 5-yr trailing annual return for ARKK is currently -1.6%. Compared to the NASDAQ 100 (20.5%) and the S&P 500 (15.0%). It seems as if Ms Wood’s Mojo has deserted her for now. Cathie Wood – 1/10; Passive US Funds – 9/10

The financial year closes and the Australian, UK and US markets are all in positive territory.

Slack Investor remains IN for all followed markets. The ASX 200 (+0.9%) and FTSE 100 (-1.3%) didn’t move much for the month. It is a continuation of good times in the US with the S&P 500 rising 4.6%. There has been a big gain in the US market this financial year of 22.7%. On top of an increase of 16.4% last financial year, Slack Investor is getting a little nervous about the US – especially after the debate last week!.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index). The quarterly updates to the Slack Portfolio have also been completed.

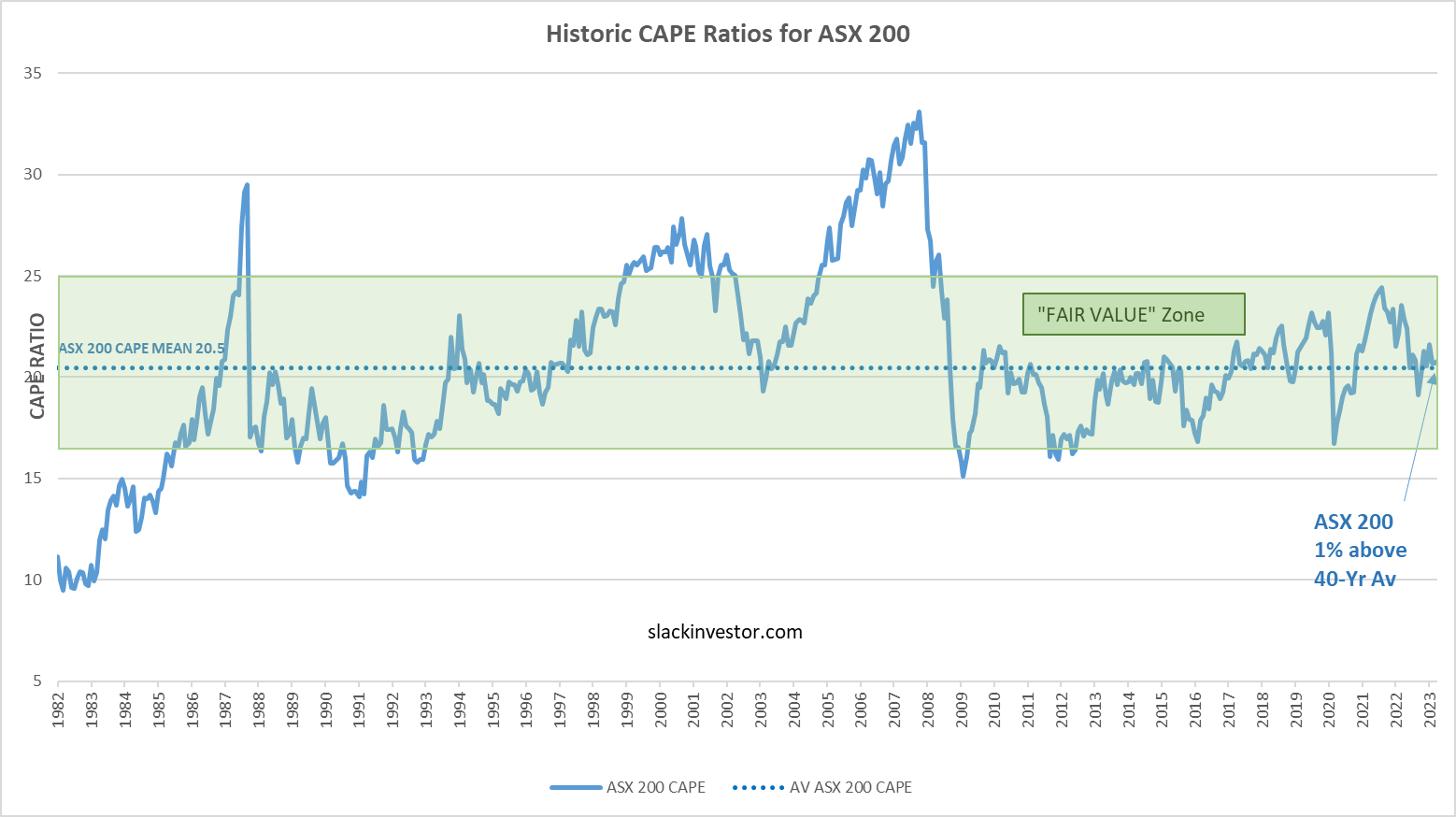

A few times a year, Slack Investor likes to take a snapshot of the markets using the Cyclically Adjusted Price to Earnings ratios (CAPE) which use ten-year average inflation-adjusted earnings. I first started using CAPE as a “value” tool in September 2021 and, my most recent look was for the end of January 2024. I have decided to do this CAPE market value analysis every few months.

Jeremy Grantham is a well known and astute investor and he argues that recent globalization has benefited the profitability of US companies and that their is good reason for an increasing CAPE trend in the US markets. However, there is some good research that links CAPE to future returns.

The CAPE (cyclically adjusted PE) ratio is not a useful timing signal for market turning points, but is a powerful predictor of long-term market returns

By plotting this CAPE over a period of time, we can look at how the whole sharemarket is currently valued in terms of historical data – this way we can track the whole share market as it oscillates between overvalued and undervalued. According to Research Affiliates, CAPE offers a negative correlation with subsequent 10-year and 20-year stock market returns – the higher the current CAPE, the lower are the expected future returns.

For the following charts, I use monthly CAPE data from Barclays, the 40-yr mean is calculated and plotted together with the latest CAPE values – up till the end of May 2024. A “fair value” zone is created in green where the CAPE is within one standard deviation of the mean (average) – click images for better resolution.

The US market remains the outlier here at 37% above its long-term value. Slack Investor is no guru, but, it doesn’t make sense to him to invest new money into a “frothy” whole-market index like the S&P 500 – at the moment!

ASX 200 Value (4% above long-term value)

FTSE 100 Value (4% below long-term value)

S&P 500 Value (37% above long-term value)

Slack Greetings from Provence – plus Navigational Tips

Evening view of the Luberon Valley, from Bonnieux, Provence. France

Slack Investor is in Europe at the moment (Boo … Hiss!), I have just finished a walking holiday in Provence, France. All I can say is that – it is a beautiful part of the world.

Steeped in history and preserved in that remarkable French way that respects the past. We moved around the intricate roads and paths using a fantastic bit of Android/IOS/Windows software called Komoot. The software is free to download on your phone with one local region – and, I added world maps for a one-time lifetime fee of $30 USD about 10 years ago – It was the best money I have ever spent, as I use the app daily. You can plot “tours” that are based upon the comprehensive “Open Street Maps” network which lists all the tiny paths and tracks that rarely appear in Google Maps. The output is best used on your phone – but the app is easier to plan using the desktop version of your Komoot account. I have no financial interest in any of the products that Slack Investor sometimes rambles on about.

Google Maps output for the area 5km east of Gordes, Provence, France – great for roads and business locationsKomoot output for the area 5km east of Gordes, Provence, France – Great for smaller roads and footpaths (tracks). The footpaths are shown as black lines and the blue line is our journey out from Gordes on the way to Roussillon.

After narrowing down my personal buying list to just 5 stocks – BetaShares NASDAQ 100 ETF (NDQ), Telix Pharmaceuticals (TLX), Technology One (TNE), Supply Network (SNL) and REA Group(REA), Slack Investor is always keen to get a second opinion – and that’s where the “fish whisperers” come in.

At this stage, I have so far bought into just one of the prospects (TLX) as, I’m hoping for a bit of a price contraction in the other stocks over the June/July period. I am not in a particular hurry to buy – as there has been recent news of “Interest cuts delayed” that might present a bit of downward pressure on stocks.

Sometimes, it makes sense to listen to the “Fish Whisperers” – those with special knowledge of the stock market. One of the financial sites that I will always look at for ideas is Livewire. Slack Investor is a subscriber to their free financial news email – just register with them. There is nothing more that I like than to saddle up to the hard work of financial experts – the hard thing, of course, is sifting through the chaff, for the wheat. But there are ways of identifying quality information – Do their methods echo with your own sound thoughts?

Let’s first have a look at Michael’s established record. He helped set up a Medallion Australian Equities Growth Fund in March last year, so there is only limited data on performance as there is a short track record. The fund growth since inception is very good (net 12-mth performance (+17.69%) – c.f ASX 200 (+10.68%) – but you would have to say that these are “early days”. Consistent long term fund performance is notoriously hard with 75% of Australian Mid to Small Cap funds underperforming the index over 10 years.

Medallion charges a management fee of 1.5% plus an outperformance fee of 20% (Oooohhh … that hurts!!) – but in fairness, their net results are, so far, exceptional – and their methodology of screening stocks looks fundamentally sound.

Long Term Compounders

These are three of the most beautiful words to Slack Investor – they exactly describe the type of stocks that I want to own. A stock that will generate growth over the long term. Let’s have a more detailed look at how the Medallion Financial Group approaches this search for long term compounders.

A consistent compounder is essentially a business that’s able to deliver consistent or persistent earnings and revenue growth over time in a reliable nature. So these are businesses that are price makers, not price takers

Michael Wayne prepared the list by screening the whole ASX for companies that have a five-year sales Compound Annual Growth Rate (CAGR) of above 5%, and a CAPE 10-year CAGR of more than 5%. Slack Investor is happy to have a further look at all of these companies.

These businesses also have a dividend per share CAGR over 10 years of more than 5%, five-year average gross margins above 10% and a five-year average return on equity over 10%. Yes Michael … keep up this research – as this is the sort of stuff that makes Slack Investor swoon!

May 2024 – End of Month Update

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

There is a bit of end of Financial year calm with the ASX 200 (+0.5%). The FTSE 100 (+1.6%) is moving on and, in a moment that seems to celebrate ex-President Trump’s guilty verdict on all 34 counts of falsifying business records, the S&P 500 moves on (+3.7%).

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

After the excitement of catching a fish there is the relatively unpleasant process of gutting the fish before things get exciting again – the cooking and the eating!

Same with stocks, the financial media is full of “darling” stocks. However, Slack Investor likes to take a deep look into the entrails before parting with his precious funds for the glorious pleasure of share ownership. The data gathering is not the most exciting part of investing and Slack Investor likes to keep things simple here – and finds the best way to sort out the worthy fish is to put them on a list with a few relevant numbers ” the guts”.

The companies that Slack Investor did a bit of research on is not definitive … I usually look into my own portfolio first to see if the investment case still stands … and, if the company has been performing well, I like to add to my holding.

The newer stocks come from a variety of sources – usually the financial press. I tend to stay away from mining and retail stocks because of the uncertainties present in these sectors. As these potential buys are a replacement for my largest portfolio member, Altium (Potential Takeover target), I have concentrated on the “growth stocks” The first screening is for growth using the CAGR and the ROIC.

Gather the Data

I have put all my prospective BUYS in a list

Company

Ticker

ROIC 23

CAGR 3-yr

Alphabet (US)

GOOGL

24

19

Altium Ltd

ALU

23

13

Audinate

AD8

12

32

Car Group

CAR

7

25

Cochlear Ltd

COH

17

14

Codan Ltd

CDA

14

9

CSL Ltd

CSL

10

13

Dicker Data

DDR

16

4

Fisher & Paykel Healthcare Corp Ltd

FPH

14

8

Microsoft (US)

MSFT

29

14

NextDC

NXT

-133

22

NVIDEA Corp (US)

NVDA

66

54

Pro Medicus

PME

50

30

REA Group Ltd

REA

20

16

Resmed

RMD

15

13

Seek Ltd

SEK

-1

-8

Supply Network

SNL

24

23

Technology One

TNE

30

13

Telix Pharmaceuticals

TLX

35

380

WiseTech

WTC

60

24

Xero

XRO

-5

23

The list needs a bit of narrowing down so I applied a filter to reduce the field to a top 10. I refined the list to those companies that have a historical ROIC of greater than 20% and a 3-yr CAGR of greater than 12% – this now becomes a list of great, profitable, efficient companies that are growing. I also added Forecast P/E ratios for 2026 from MarketScreener.

Company

Ticker

ROIC 23

CAGR 3-yr

P/E 2026

NVIDEA Corp (US)

NVDA

66

54

26

WiseTech

WTC

60

24

60

Pro Medicus

PME

50

30

82

Telix Pharmaceuticals

TLX

35

380

35

Technology One

TNE

30

13

33

Microsoft (US)

MSFT

29

14

26

Alphabet (US)

GOOGL

24

19

18

Supply Network

SNL

24

23

21

Altium Ltd

ALU

23

13

45

REA Group Ltd

REA

20

16

36

The Price/Earnings Filter

The above list represents some profitable, growing companies – but they might be priced too highly. Slack Investor generally doesn’t like to pay for a forecast P/E ratio of over 40 when I’m buying a new growth stock – that means the projected earnings are 40 times the current price of the stock. This reduces the table to 7 stocks. I can reduce the table even further by taking out the 3 US based stocks (MSFT, NVDA, GOOGL) – which I can buy in one trade by purchasing more of the ASX listed NDQ . The Betashares NASDAQ 100 ETF was already on my BUY radar. Have a look at the 1-yr returns on these amazing growth companies in the table below of top NDQ holdings – It is unlikely that this stellar growth will continue … but there is certainly momentum here.

BetaShares NASDAQ 100 ETF (NDQ) top ten holdings – Morningstar

The Final List – this is not advice!

Company

Ticker

ROIC 23

CAGR 3-yr

P/E 2026

Price

Telix Pharmaceuticals

TLX

35

380

35

$15.05

Technology One

TNE

30

13

33

$16.25

Supply Network

SNL

24

23

21

$20.05

REA Group Ltd

REA

20

16

36

$179.64

Betashares NASDAQ 100

NDQ

–

18

27 (2024)

$41.35

As well as BetaShares NASDAQ 100 ETF (NDQ), I will be looking forward to topping up my supplies of Technology One, Supply Network and REA Group and hoping for a bit of a price contraction over the next couple of months. The share price shown in this table is at the end of April 2024.

A newcomer to this list is Telix Pharmaceuticals (TLX) – a relatively new entry to the ASX that develops radiopharmaceuticals for cancer diagnosis and treatment. There is a lot of talk of this companies potential.

“It’s developing into a premier global radiopharmaceutical company … I see this as going on to become the next CSL in Australia.”

A CAGR of 380 is skewed by recent figures – but they definitely are a growth company – but there is risk here! Slack Investor will roll the dice and add a bit of this to his portfolio while it is still around the $15 mark – there is a bit of momentum with this stock – might have to get in soon! He likes that they already have a money-making product and they have a further product pipeline ready to roll out.

(Telix Pharmaceuticals) has demonstrated extraordinary progress by generating over $100 million in revenue in the March 2023 quarter, a remarkable leap from zero, less than twelve months ago.

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

A bit of the froth has settled down with the ASX 200 (-2.9%) and the S&P 500 (-4.2%). However, the FTSE 100 (+2.4%) is powering on at the moment. After a while in the doldrums, the FTSE 100 is now reaching record highs with the expectation of some interest rate cuts soon.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

{kind=link}