A few times a year, Slack Investor likes to take a snapshot of the markets using the Cyclically Adjusted Price to Earnings ratios (CAPE) which use ten-year average inflation-adjusted earnings. I first started using CAPE as a “value” tool in September 2021 and, my most recent look was for the end of January 2024. I have decided to do this CAPE market value analysis every few months.

Jeremy Grantham is a well known and astute investor and he argues that recent globalization has benefited the profitability of US companies and that their is good reason for an increasing CAPE trend in the US markets. However, there is some good research that links CAPE to future returns.

The CAPE (cyclically adjusted PE) ratio is not a useful timing signal for market turning points, but is a powerful predictor of long-term market returns

By plotting this CAPE over a period of time, we can look at how the whole sharemarket is currently valued in terms of historical data – this way we can track the whole share market as it oscillates between overvalued and undervalued. According to Research Affiliates, CAPE offers a negative correlation with subsequent 10-year and 20-year stock market returns – the higher the current CAPE, the lower are the expected future returns.

For the following charts, I use monthly CAPE data from Barclays, the 40-yr mean is calculated and plotted together with the latest CAPE values – up till the end of May 2024. A “fair value” zone is created in green where the CAPE is within one standard deviation of the mean (average) – click images for better resolution.

The US market remains the outlier here at 37% above its long-term value. Slack Investor is no guru, but, it doesn’t make sense to him to invest new money into a “frothy” whole-market index like the S&P 500 – at the moment!

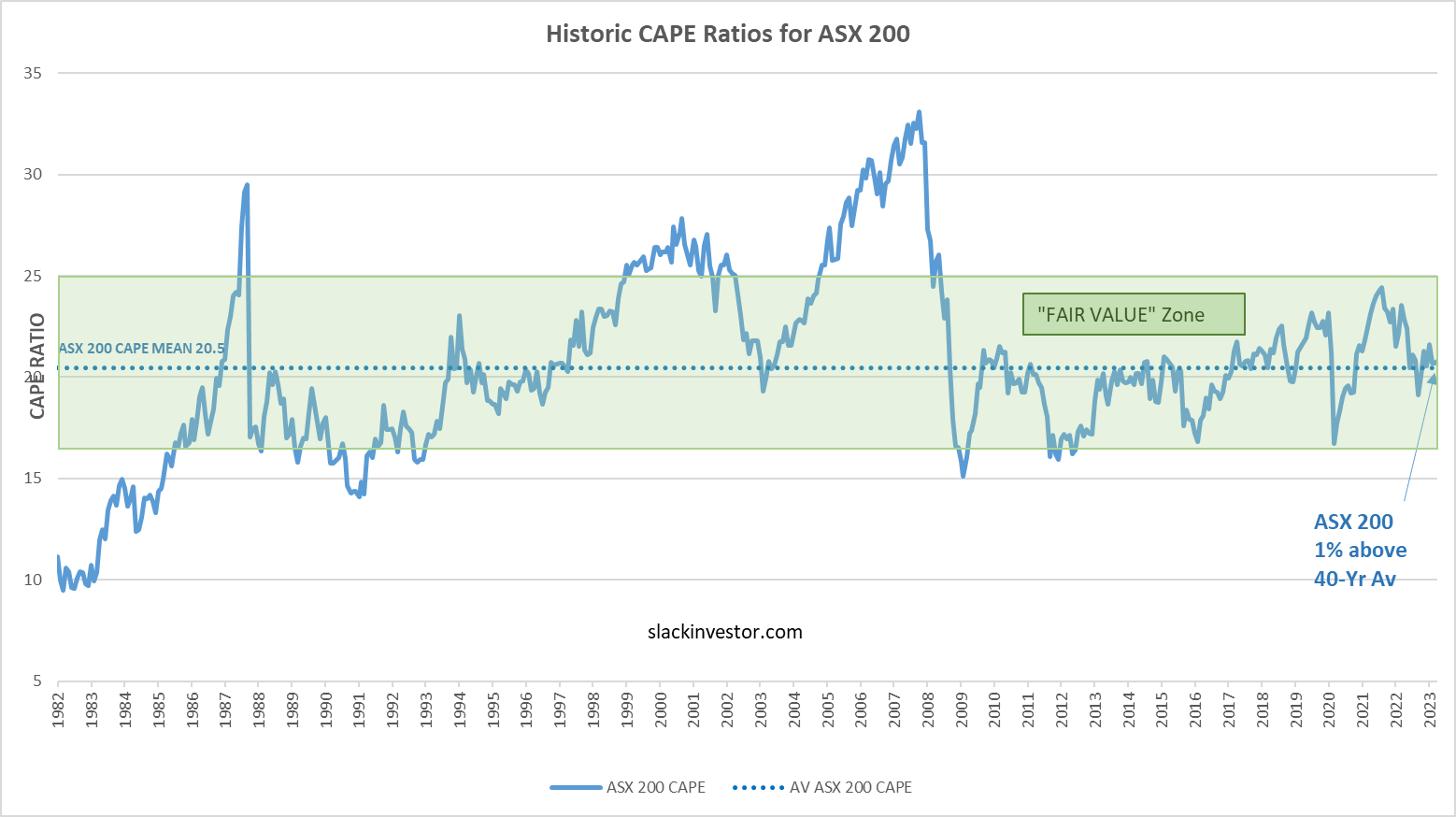

ASX 200 Value (4% above long-term value)

FTSE 100 Value (4% below long-term value)

S&P 500 Value (37% above long-term value)

Slack Greetings from Provence – plus Navigational Tips

Evening view of the Luberon Valley, from Bonnieux, Provence. France

Slack Investor is in Europe at the moment (Boo … Hiss!), I have just finished a walking holiday in Provence, France. All I can say is that – it is a beautiful part of the world.

Steeped in history and preserved in that remarkable French way that respects the past. We moved around the intricate roads and paths using a fantastic bit of Android/IOS/Windows software called Komoot. The software is free to download on your phone with one local region – and, I added world maps for a one-time lifetime fee of $30 USD about 10 years ago – It was the best money I have ever spent, as I use the app daily. You can plot “tours” that are based upon the comprehensive “Open Street Maps” network which lists all the tiny paths and tracks that rarely appear in Google Maps. The output is best used on your phone – but the app is easier to plan using the desktop version of your Komoot account. I have no financial interest in any of the products that Slack Investor sometimes rambles on about.

Google Maps output for the area 5km east of Gordes, Provence, France – great for roads and business locationsKomoot output for the area 5km east of Gordes, Provence, France – Great for smaller roads and footpaths (tracks). The footpaths are shown as black lines and the blue line is our journey out from Gordes on the way to Roussillon.

After narrowing down my personal buying list to just 5 stocks – BetaShares NASDAQ 100 ETF (NDQ), Telix Pharmaceuticals (TLX), Technology One (TNE), Supply Network (SNL) and REA Group(REA), Slack Investor is always keen to get a second opinion – and that’s where the “fish whisperers” come in.

At this stage, I have so far bought into just one of the prospects (TLX) as, I’m hoping for a bit of a price contraction in the other stocks over the June/July period. I am not in a particular hurry to buy – as there has been recent news of “Interest cuts delayed” that might present a bit of downward pressure on stocks.

Sometimes, it makes sense to listen to the “Fish Whisperers” – those with special knowledge of the stock market. One of the financial sites that I will always look at for ideas is Livewire. Slack Investor is a subscriber to their free financial news email – just register with them. There is nothing more that I like than to saddle up to the hard work of financial experts – the hard thing, of course, is sifting through the chaff, for the wheat. But there are ways of identifying quality information – Do their methods echo with your own sound thoughts?

Let’s first have a look at Michael’s established record. He helped set up a Medallion Australian Equities Growth Fund in March last year, so there is only limited data on performance as there is a short track record. The fund growth since inception is very good (net 12-mth performance (+17.69%) – c.f ASX 200 (+10.68%) – but you would have to say that these are “early days”. Consistent long term fund performance is notoriously hard with 75% of Australian Mid to Small Cap funds underperforming the index over 10 years.

Medallion charges a management fee of 1.5% plus an outperformance fee of 20% (Oooohhh … that hurts!!) – but in fairness, their net results are, so far, exceptional – and their methodology of screening stocks looks fundamentally sound.

Long Term Compounders

These are three of the most beautiful words to Slack Investor – they exactly describe the type of stocks that I want to own. A stock that will generate growth over the long term. Let’s have a more detailed look at how the Medallion Financial Group approaches this search for long term compounders.

A consistent compounder is essentially a business that’s able to deliver consistent or persistent earnings and revenue growth over time in a reliable nature. So these are businesses that are price makers, not price takers

Michael Wayne prepared the list by screening the whole ASX for companies that have a five-year sales Compound Annual Growth Rate (CAGR) of above 5%, and a CAPE 10-year CAGR of more than 5%. Slack Investor is happy to have a further look at all of these companies.

These businesses also have a dividend per share CAGR over 10 years of more than 5%, five-year average gross margins above 10% and a five-year average return on equity over 10%. Yes Michael … keep up this research – as this is the sort of stuff that makes Slack Investor swoon!

May 2024 – End of Month Update

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

There is a bit of end of Financial year calm with the ASX 200 (+0.5%). The FTSE 100 (+1.6%) is moving on and, in a moment that seems to celebrate ex-President Trump’s guilty verdict on all 34 counts of falsifying business records, the S&P 500 moves on (+3.7%).

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

Slack Investor likes the quiet life, and doesn’t usually go looking for trouble, but a recent birthday put me at 67 – this is the age threshold for the Australian Aged Pension. Other than feeling old, this is not too much of a concern as I am a happy self-funded retiree.

However, in a generous flourish, the previous government made it much easier for self-funded retirees to qualify for the Commonwealth Seniors’ Health Card (CSHC). This card provides savings on some Pharmacy costs and gives easier access to higher rates of reimbursement for out of pocket expenses (Medicare Safety Net). Some GP’s will offer bulk-billing to CSHC holders as they can get a higher Medicare fee for these consultations. So, this card looks worth the effort if you qualify and, looking at the new numbers, most retirees not on the pension, would.

Age pension age and an Australian citizen? The critical test is your income … and not just any income … but your “Adjusted income”.

To meet the income test, your “Adjusted Income” must be less than the following:

$95,400 a year if you’re single

$152,640 a year for couples

$190,800 a year for couples separated by illness, respite care or prison.

These values are valid for 2024 and they get inflation adjusted each year

For Slack Investor, it was a matter of gathering scans of our most recent ATO Notice of Assessment for my partner and myself. Plus contacting my Super Provider to send me an income schedule for each of my Pension accounts – These are known as form SA 330 and are often requested for dealing with Centrelink, DVA, etc.

As we do not own an investment property, the only inputs to our Adjusted Income were our taxable incomes and deemed income from our account based pensions.

Any money in our accumulation accounts or bank accounts was not considered in our deemed “Adjustable Income” as a couple.

Noel Whittaker provides a handy calculator to work out your total deemed income from your pension assets (Currently about 2% of assets). I stress it is not the actual income from these pensions that is relevant – but the deemed income! The asset amounts of our pensions (Estimated for the application date – from your super fund or SMSF) were put into Noel’s Calculator. As the total of our deemed pension income plus our taxable incomes was under the $152,640 a year for couples, we proceeded with the application online through MyGov/Centrelink/Make a Claim or Review Claim Status. This is where the fun begins.

Handy Tips

Before applying, get some identification documents ready and your latest ATO Notice of Assessment (in pdf form). Make sure you have a MyGov account and have Centrelink linked to it. I used the online form to apply, and it was frustrating at times, but generally OK. Others have downloaded the form, filled it out and taken it to Centrelink for checking.

Contact your Super Funds for a SA 330 schedule that will give you relevant details of any Account-Based Pension that you own for the last tax year.

If you have a SMSF, contact your provider and they will furnish you with information on each of your pension funds. You will then have to download and fill out your own SA 330, as a trustee, for each of your income streams.

At one of the forms sticking points, I found the video on the application process by Brendan Ryan of Later Life Advice very useful – worth a watch for a 22 minute overview of this process (the video is found in the top left third of the page).

I must warn that this application is not for the feint-hearted – But do not give up! If you are having trouble, book an appointment with Centrelink – They will also check your documents if you are not sure.

The complexities of dealing with Centrelink and the CSHC have been entertainingly documented in the SMH and YourLifeChoices. There were several points where I was having what my mother would describe as “Sailor’s Talk” with my computer.

For all the frustration and “dead ends” encountered during the application process, I found a strategy of “Walk away – and try again another day” did the trick. Although, I will not find out about whether my application will be successful till July 2024, I did learn something useful along the way … How to Edit pdf forms – which came in handy as SMSF trustees have to populate several SA 330 forms with mostly the same data.

Using Google Chrome to fill out PDF forms

I don’t have any form-filling PDF software (e.g. Adobe Acrobat full version) and I am reluctant to install the “free” clients that usually come with some adware or a trial period. I was delighted to find out that this form-filling task can be done in my Chrome browser without installing anything extra. Locate the PDF you want to edit in File Browser.

Right-Click the file to open up the context menu – Scroll down to “Open with” a new dialogue box will open showing Google Chrome if you have it. Select “Google Chrome”.

The form will then open as a Chrome Tab and you can edit away then save or print your changes (Download and Print Symbol at top right of the Chrome tab).

After the excitement of catching a fish there is the relatively unpleasant process of gutting the fish before things get exciting again – the cooking and the eating!

Same with stocks, the financial media is full of “darling” stocks. However, Slack Investor likes to take a deep look into the entrails before parting with his precious funds for the glorious pleasure of share ownership. The data gathering is not the most exciting part of investing and Slack Investor likes to keep things simple here – and finds the best way to sort out the worthy fish is to put them on a list with a few relevant numbers ” the guts”.

The companies that Slack Investor did a bit of research on is not definitive … I usually look into my own portfolio first to see if the investment case still stands … and, if the company has been performing well, I like to add to my holding.

The newer stocks come from a variety of sources – usually the financial press. I tend to stay away from mining and retail stocks because of the uncertainties present in these sectors. As these potential buys are a replacement for my largest portfolio member, Altium (Potential Takeover target), I have concentrated on the “growth stocks” The first screening is for growth using the CAGR and the ROIC.

Gather the Data

I have put all my prospective BUYS in a list

Company

Ticker

ROIC 23

CAGR 3-yr

Alphabet (US)

GOOGL

24

19

Altium Ltd

ALU

23

13

Audinate

AD8

12

32

Car Group

CAR

7

25

Cochlear Ltd

COH

17

14

Codan Ltd

CDA

14

9

CSL Ltd

CSL

10

13

Dicker Data

DDR

16

4

Fisher & Paykel Healthcare Corp Ltd

FPH

14

8

Microsoft (US)

MSFT

29

14

NextDC

NXT

-133

22

NVIDEA Corp (US)

NVDA

66

54

Pro Medicus

PME

50

30

REA Group Ltd

REA

20

16

Resmed

RMD

15

13

Seek Ltd

SEK

-1

-8

Supply Network

SNL

24

23

Technology One

TNE

30

13

Telix Pharmaceuticals

TLX

35

380

WiseTech

WTC

60

24

Xero

XRO

-5

23

The list needs a bit of narrowing down so I applied a filter to reduce the field to a top 10. I refined the list to those companies that have a historical ROIC of greater than 20% and a 3-yr CAGR of greater than 12% – this now becomes a list of great, profitable, efficient companies that are growing. I also added Forecast P/E ratios for 2026 from MarketScreener.

Company

Ticker

ROIC 23

CAGR 3-yr

P/E 2026

NVIDEA Corp (US)

NVDA

66

54

26

WiseTech

WTC

60

24

60

Pro Medicus

PME

50

30

82

Telix Pharmaceuticals

TLX

35

380

35

Technology One

TNE

30

13

33

Microsoft (US)

MSFT

29

14

26

Alphabet (US)

GOOGL

24

19

18

Supply Network

SNL

24

23

21

Altium Ltd

ALU

23

13

45

REA Group Ltd

REA

20

16

36

The Price/Earnings Filter

The above list represents some profitable, growing companies – but they might be priced too highly. Slack Investor generally doesn’t like to pay for a forecast P/E ratio of over 40 when I’m buying a new growth stock – that means the projected earnings are 40 times the current price of the stock. This reduces the table to 7 stocks. I can reduce the table even further by taking out the 3 US based stocks (MSFT, NVDA, GOOGL) – which I can buy in one trade by purchasing more of the ASX listed NDQ . The Betashares NASDAQ 100 ETF was already on my BUY radar. Have a look at the 1-yr returns on these amazing growth companies in the table below of top NDQ holdings – It is unlikely that this stellar growth will continue … but there is certainly momentum here.

BetaShares NASDAQ 100 ETF (NDQ) top ten holdings – Morningstar

The Final List – this is not advice!

Company

Ticker

ROIC 23

CAGR 3-yr

P/E 2026

Price

Telix Pharmaceuticals

TLX

35

380

35

$15.05

Technology One

TNE

30

13

33

$16.25

Supply Network

SNL

24

23

21

$20.05

REA Group Ltd

REA

20

16

36

$179.64

Betashares NASDAQ 100

NDQ

–

18

27 (2024)

$41.35

As well as BetaShares NASDAQ 100 ETF (NDQ), I will be looking forward to topping up my supplies of Technology One, Supply Network and REA Group and hoping for a bit of a price contraction over the next couple of months. The share price shown in this table is at the end of April 2024.

A newcomer to this list is Telix Pharmaceuticals (TLX) – a relatively new entry to the ASX that develops radiopharmaceuticals for cancer diagnosis and treatment. There is a lot of talk of this companies potential.

“It’s developing into a premier global radiopharmaceutical company … I see this as going on to become the next CSL in Australia.”

A CAGR of 380 is skewed by recent figures – but they definitely are a growth company – but there is risk here! Slack Investor will roll the dice and add a bit of this to his portfolio while it is still around the $15 mark – there is a bit of momentum with this stock – might have to get in soon! He likes that they already have a money-making product and they have a further product pipeline ready to roll out.

(Telix Pharmaceuticals) has demonstrated extraordinary progress by generating over $100 million in revenue in the March 2023 quarter, a remarkable leap from zero, less than twelve months ago.

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

A bit of the froth has settled down with the ASX 200 (-2.9%) and the S&P 500 (-4.2%). However, the FTSE 100 (+2.4%) is powering on at the moment. After a while in the doldrums, the FTSE 100 is now reaching record highs with the expectation of some interest rate cuts soon.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

Slack Investor is always on the lookout for growth companies … particularly when he is on the BUY! Since retirement, I haven’t had much chance to be on the Buy side of a transaction lately – as there isn’t that flow of fresh new money coming into the coffers from employment. Pre-retirement, any new money would flow into the cash reserves of my Super (SMSF -Self Managed Super Fund). When a sufficient amount of cash had built up, I would look around for some company shares to buy.

However, with the expected inflow of a bit of cash with the impending sale of Altium, I am starting to look around for suitable receivers of Slack Investor loot. Slack Investor is “Going Fishing”. The first thing I want in my pond is profitable companies – but I also want them to have a record of growth. In the second part of this fishing series, I will try to narrow things down to companies that I would actually like to buy.

Measures of Profitability

Slack Investor likes a company, that he invests in, to not only make a profit – but to use its shareholder funds in the best way to make a profit. There are many ways to look at profitability, but Slack Investor is pretty lazy in this regard and you won’t find him forensically gazing over profit and loss statements from a company report. I prefer couple of simple ratios to get an overview – I am no expert accountant.

Return on Equity (ROE)

ROE = Net Income/Shareholder Equity

I have always used Return on Equity (ROE) as a simple measure to give an idea on how a company is growing. Strictly speaking, the ROE is more a measure of profitability and how well it grows each dollar of company funds.

The higher the ROE, the more efficient a company’s management is at generating income and growth from its equity financing.

This metric is very easy to find in market aggregator sites such as Yahoo.com, Morningstar, or Investing.com. For a deep dive, I prefer Marketscreener.com – which has the advantage of showing Predicted ROE for the next few years on each companies financial page. One of the problems with ROE is that, companies with debt can present an inflated ROE.

Return on Invested Capital (ROIC)

ROIC = Net Profit (After Tax)/Average Invested Capital

The purest way of looking at how good a company is in converting shareholders money into profit is the ROIC. Unfortunately, this figure is harder to come by on the generic financial aggregator sites. This ratio is superior to the ROE as it accounts for the debt levels of a company – as the Average Invested Capital is the Average Equity – Average Debt.

Measure of Growth

Compound annual growth rate (CAGR)

A quick way of determining if a company is growing is the CAGR. It is often constructed from past , data. The “Compound Annual Growth Rate”—is the annualized rate of growth in the value of the Earnings, or Revenue, over a stated period. The maths is a bit complicated and best done on a spreadsheet or a search around the financial sites. I found limited CAGR data for stocks at Morningstar and finbox.com

CAGR is defined as the annualized growth rate in the value of a financial metric – such as revenue and EBITDA – or an investment across a specified period.

Fortunately there are some really nice blokes in the financial world that share the burden of responsibility to educate people about the share market as well as operating a profitable business. A shout out to Owen Raszkiewicz of the RASK Group. A great place to start your financial education with Owen is his Australian Finance podcast that he co-hosts with Kate Campbell. Slack Investor will often tune in to their discussions.

Below is a table Owen prepared in August 2023 that ranks Australian stocks in terms of their profitability (ROIC – Return on Invested Capital – Column F). He also shows, in the last column, the stock’s historical growth rate for the 5 years 2017-2022.

From Rask Media – ASX’s best companies published August 2023 – ranked in order of ROIC- Click on image to enlarge

This is a great place to start fishing, metrics for profitability and growth in one place. Pro Medicus is standing out here – High profitability (ROIC 55.48%) and high historical growth (5-yr CAGR 24.22%). A complete picture needs both of these metrics. For example, Woolworths has a high profitability (ROIC 41.28%) but is laggard in historical growth (5-yr CAGR 2.10%).

The next article in this series will look at how Slack Investor narrows these stocks down and then screens them further with the P/E Ratio to try to make sure that each potential buying stock is not overpriced.

Renesas CEO Hidetoshi Shibata (left) and Altium CEO Aram Mirkazemi (right) firming up the takeover deal – From Business News Australia.

It is with very mixed feelings that Slack investor reports on the likely takeover of Altium (ALU) – one of his major holdings (16.6% of total Portfolio) – by the Japanese Renesas Electronics Corporation.

Renesas will acquire all outstanding shares of Altium for a cash price of A$68.50 per share, representing a total equity value of approximately A$9.1 billion

Although this represents a tidy profit, as I first bought into Altium about 10 years ago when they were trading at $3.30, I will be genuinely sad to stop being a shareholder of this wonderful company. I envisaged holding Altium shares for a very, very, long time!

Slack Investor’s 10-yr journey as an Altium shareholder – Monthly price chart from incrediblecharts.com – click chart for better resolution

Why I originally bought into Altium?

Let’s get this straight, Slack Investor is no stock picking genius. My portion of profitable sold shares is only about 55%. That is, I have made losses on 45% of them – it is not that impressive! – but my overall performance results are good. This is because I follow the Peter Lynch philosophy – where you try to stay in the stocks that are performing well and “weed out” the stocks that are not doing well.

“Some stocks go up 20-30 percent – and they get rid of it and hold onto the dogs. And it’s sort of like watering the weeds and cutting out the flowers. You want to let the winners run.”

Peter Lynch – Legendary Investor and Fund Manager. From 1977 until 1990, he ran the Magellan fund where he averaged a 29.2% annual return for those years.

Slack Investor is always on the lookout for growth companies … and Altium poked up its head and looked at me in 2014 from one of the financial sites that I read. The next step is a bit of independent research. My “go to” here is the most excellent Market Screener site. I went through my usual process for buying and checked the Market Screener/Financials tab for a reasonable projected Price/Earnings ratio, an established record of improvement in earnings, and a forecast Return on Equity (ROE) above 15%. Altium stood out here with no debt and a ROE of between 35 and 50. This company was growing!

After my initial purchase, I bought more parcels of ALU over the next two years as the shares continued to grow and their outlook projections were confirmed.

The Altium Story

Altium is an Australian-based software company that provides electronics design software to circuit-board engineers. These circuit boards are in every bit of technology that we own.

By the time Slack Investor had woken up to the Altium story, Aram Mirkazemi was the established CEO of Altium Limited. He came to Australia from Iran as a refugee in the 1980’s after a 6-month stint in a refugee camp in Pakistan. He did not speak English. After gaining qualifications in IT and engineering, he met Nick Martin, the founder of Altium, at a soccer game and Nick offered him a job. After an eventual falling out, Aram left to start his own software company. When Nick steeped down as CEO, Aram returned to Altium with a vision to make Altium a world player in printed circuit board design.

… in order to be able to change the way the electronics industry works you need to be able to standardise on one platform, like the graphics industry did with Photoshop or Microsoft’s dominance of the operating system and productivity tools market.

After several years of growth and gaining market share. The Altium board rejected an offer of $38.50 per share from Autodesk Inc back in June 2021 as they thought that the offer ‘significantly undervalues’ the companies prospects. The 2024 Renesas offer is yet to be approved by shareholders, but it seems that all the significant players are already “on board”. The offer A$68.50 per share in cash. represents a premium of approximately 34% to the pre-offer price.

All I can say is, it has been an honour to be part-owner (shareholder) of this great company – Thank you Aram and his team. I will be selling part of my holding this tax year (to spread the capital gain over two tax years) and wait for the cash offer to come through in 2025 for the remainder.

March 2024 – End of Month Update

More Happy Days in the stock market. As the troubled world marches on, all Slack Investor followed markets rose this month. The ASX 200 up 2.6%, the FTSE 100 up 4.2%, and the S&P 500 up 3.1%,

Slack Investor remains IN for the FTSE 100, the ASX 200, and the US Index S&P 500.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index). The quarterly updates to the Slack Portfolio have also been completed.

After discussing how hard it is for those trying to buy their first home. Slack Investor is compelled to provide some hope in the desire to own your home before you retire. The numbers are in … and, not owning a house in retirement or, losing your job before you retire, puts you at real risk of not reaching a comfortable financial position.

Whereas very few retired home owners are in poverty, most retired renters are …

There are very few existing incentives on the dusty twisted road to home ownership. They include Stamp Duty exemptions/concessions that vary from state to state. In Victoria, they are available for homes less than $750K. There is also the First Home Buyers Grant (FHBG), which, again, is dependent on which state you live. In Victoria, that comes in at a measly (but I’ll take it!) $10K.

All of these things are worth considering and applying for when you finally purchase a home, but the First Home Super Saver Scheme (FHSSS) is a lesser known arrangement that seems to make sense – but it requires a bit of “setting up”.

In order to make the most of the FHSSS, you’ll need to start planning well ahead of the time to buying a house/apartment (3 – 4 years?) – But planning ahead is the very trait that Slack Investor loves!

First Home Super Saver Scheme (FHSSS)

I did refer to the First Home Super Saver Scheme (FHSSS) way back in 2017 when it was just a twinkle in ScoMo’s eye – it started as an election promise to get the “young folk” on board as the government felt a need to at least be seen to be doing something to help first homeowners.

These voluntary contributions can be withdrawn from your super when you finally ready to purchase a home – by filling out an ATO form for a ‘determination’. The determination will tell you exactly how much you can withdraw – it will be a little more than you have put in (your contributions – up to $50K – plus deemed earnings)- and waiting a month.

Getting the money out usually takes 15–25 business days … once you withdraw money to buy a house, you have one year to use it

These extra contributions are over and above the compulsory super that your employer makes. The scheme works by making an arrangement with your paymaster to salary sacrifice into your super – up to $15K per tax year. Contributions can also be made by arranging with your super provider to make a personal super contribution.

The tax savings come about as, you only pay 15% tax on these super contributions – rather than your marginal rate of say, 32.5%. Plug in your own details into this calculator to determine your possible tax savings.

I would recommend all prospective home owners to take a look at this scheme. Assessment for eligibility is made on an individual basis … so couples and friends can combine their amounts – but start now – it will take a few years to get a useful house deposit.

Colonial First State outline a case study of a couple that have each started voluntary extra super contributions of $15K – After 15% tax this comes down to $12 750 p.a of contributions into their funds. After 4 years, they each have amassed $55K (4 x $12 750 plus deemed interest). A combined house deposit of $110K was possible using the FHSSS – and, using a favourite Slack Investor way of saving – deductions from your salary before you even see it! All of this with tax advantages.

Homework (get it!): – Potential homeowners – read about it – and get on the FHSSS!

Even Superman has his limits – Is it Kryptonite OR Brussell Sprouts?

Slack Investor writes a lot about Superannuation because it is a fantastic component to have in your armoury to establish financial independence – in a tax-effective way.

The ultimate aim for Slack Investor is to fund your own retirement, but in reality, according to the Association of Superannuation Funds of Australia (ASFA) estimates, a minority (43% ) of Australians of retirement age would be self-funded by 2023 – this percentage should increase as the compulsory superannuation system matures.

Before we get to this mix, by the time you retire, you do want to have a place to live and be free of landlords. This may sound impossible to some at the moment – but it is a vital part of financial independence. It can be a “tiny home”, an apartment, a place in a regional area …. as long as it is yours!

Tiny Homes – This 20 sq m little bewdy will set you back $32 000 – however, you still have to find land for it – and connect to services.

It is so important to aim to own your own home by the time that you retire – even if it is a 1-br apartment. Admittedly, this is so much harder than it used to be! Looking at the figures below, it is vital to get as large a home deposit as you can to reduce your borrow amount – this should be one of your early financial goals. However, without help, a multi-bedroom home near a capital city now seems near impossible.

If you dont have a deposit, October 2023 data showed that Australians need an income of more than $300,000 a year to buy a median priced home. Household incomes required were considerably less, but still “eye watering”, for outer suburbs and regional cities. e.g. Geelong $243,333, Brisbane $223,333. Apartments are usually less expensive – and require less income to service the home loan.

At its most basic level, superannuation is forced retirement savings for all working Australians. A compulsory contribution of 11.5% of your salary (from 1 July 2024) that will compound till your preservation age (between 55 and 60).

According to Treasury projections, about 60% of retirees will have less than $250 000 in super in 2024. This amount of super is not enough to fund a comfortable retirement. $250 000 in pension mode at the official Age 67 drawdown rate of 5% generates only $12 500 income per year. Clearly, many Australians will need to rely on a mix of their super and the aged pension for retirement income. The Aged Pension is available to Australians over 67 – but, it is means tested.

The bare minimum to aim for is the “sweet spot” in the aged pension asset test where your assets are a bit more than the maximum allowed for the full pension. Under current rules (2024), home owning couples can have $451 500 in assets (singles $301 750) and still qualify for the full government aged pension (at age 67).

In 2020, the Alliance for a Fairer Retirement System pointed to a super sweet spot of around $400,000, which can see a pensioner (home-owning) couple “earning $1,000 a month more than a couple with $800,000 in savings.”

The first chart shows 20 different amounts of superannuation that you might have saved up by the time you are ready to retire – ranging from $150 000 to $1 100 000 above chart – from saveoursuper.org.au.

This next chart is far more interesting, it shows your total income from different amounts of superannuation (shown in the above table) mixed with the aged pension – for a home owning couple. For simplicity, these tables assume your only non-home assets are in super and the aged pension rates were those applicable in 2021 ($34 777 per couple). The essence of the table is still valid.

Total amount of retirement income – for a home owning couple – Combination of Part-Aged Pension (orange) and 5% of Superannuation Balance (Blue) for each of the 20 amounts of Superannuation Balance shown in the first chart (Using data for 2020/21)- saveoursuper.org.au

Bizarrely, there is a point on the total retirement-income (couple) table corresponding to around $400 000 in assets/super where an increased assets/super balance does not lead to an increased total income due to the asset test pension taper rate. Above that point, for those on the part-pension/super mix, the more super you have, your total income actually goes down. This strange anomaly exists for assets/super between $400 000 and $800 000 (2021/2020 data).

Clearly, the current assets test to qualify for the aged pension is unfair and provides a disincentive to save -and should be changed. But, until then, a major retirement goal is to use your super to get your total assets to near the sweet spot before you reach age 67.

(It)is not fair that people who forgo consumption and save more to increase their living standards in retirement and reduce their reliance on an Age Pension should instead get less retirement income. This is the perverse outcome for a large range of savings under the 2017 assets test.

How the Assets test works (in real life) for the aged pension (2024 Data)

According to Services Australia, for the aged pension, assets are property or items you or your partner own in full or part – this does not include your home! It does include Financial Investments (Bank accounts, shares, managed funds, annuities, etc), Personal assets (Home contents and vehicles), Superannuation and Real Estate.

I had a recent example of filling in an assets form for a close relative. Her bank statements and investments were easy to quantify. We were advised that personal assets should be valued according to what we could get if we were “keen sellers”. It was suggested to us that, other than vehicles, most peoples personal effects would amount to between $5000 and $10 000. This proved to be near the mark as most furniture and home items end up having to be donated when finalizing a deceased estate.

For the table below, the aged pension and asset limits are current values* and correct at February 2024. Using 2024 data, the “sweet spot” for assets is now near $451 500 for couples ($301 750 for singles). If you had $250 000 in super, and your “other assets” added up $60 000 (Car $13 000, Bank Ac’ts/Shares/Funds $35 000, Home Contents $12 000). Your Total assets would be $310 000.

For a couple with similar “other assets” and a combined super of $400 000, your total assets would be $460 000.

Situation

Asset Limit

Other Assets*

Super

Drawdown from Super@ 5%

Age Pension

Total Income

Single Home-owner

$301 750

$60 000

$250 000

$12 500

$28 514

$41 014

Couple Home-owner (Combined)

$451 500

$60 000

$400 000

$20 000

$42 988

$62 988

Table based on a single home-owner with $310 000 total assets ($60K + $250K) and a couple home-owners with $460 000 total assets ($60K + $400K) – using Feb 2024 values for the Aged Pension and Asset Limits.

Using this mix of super and the pension, when reaching the pension qualifying age , a modest to comfortable retirement is possible under current rules when you own your own home. Also, under the Work Bonus Rules, singles can earn up to $5304 (Couples $9360) in a part-time job without affecting their aged pension.

Comfortable lifestyle (p. a.)

Modest lifestyle (p. a.)

Couple $71,723

Couple $46,620

Single $50981

Single $32,417

ASFA calculated annual retirement requirements for those aged 65-84 (September quarter 2023) for both “comfortable” and “modest” lifestyles

February 2024 – End of Month Update

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

Little movement this month for the ASX200 (+0.2%) – but, it is testing new all-time highs. Nothing happening with the FTSE 100 (0.0%) at the moment.

The S&P 500 (+5.2) and the NASDAQ 100 are hitting new record highs and Slack Investor is pleased to go with the momentum but remains nervous for these markets.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

A few times a year, Slack Investor likes to take a snapshot of the markets using the Cyclically Adjusted Price to Earnings ratios (CAPE) which use ten-year average inflation-adjusted earnings. I first started using CAPE as a “value” tool in September 2021 and, my most recent look was in mid-November 2023. I have decided to do this CAPE market value analysis every 3 months – as I like to keep a feel of where we are – as the market cycles. The next update will be in mid-May 2024.

By plotting this CAPE over a period of time, we can look at how the whole sharemarket is currently valued in terms of historical data – this way we can track the whole share market as it oscillates between overvalued and undervalued.

Using monthly CAPE data from Barclays, the 40-yr mean is calculated and plotted together with the CAPE values. A “fair value” zone is created in green where the CAPE is within one standard deviation of the mean (average).

ASX 200 Value

Historic CAPE ratios for the ASX 200 – From 1982 to end of January 2024 – Click the chart for better resolution.

FTSE 100 Value

Historic CAPE ratios for the FTSE 100 – From 1982 to end of January 2024– Click the chart for better resolution.

S&P 500 Value

Historic CAPE ratios for the S&P 500 – From 1982 to end of January 2024 – Click the chart for better resolution.

At the end of January 2023, the FTSE 100 (11% below the 40-yr average) is the only followed market “ON SALE”. I love a price reduction!

The ASX 100 (4% above the 40-yr average) is in the “Fair Value” zone. However, the S&P 500 still looks well overvalued at 32% above the 40-yr average – and has just moved above the “Fair Value” zone.

Slack Investor usually just assesses stock market returns at the end of the financial year. However, calendar year 2023 was some ride.

The 2023 ASX 200 Chart

For the 2023 calendar year, the ASX 200 Index started at 7020, and ended up at 7590 – a 12-mth increase of about 8% – but, on the way, it fell to a year low of 6751 – a temporary fall of 3.8%.

Of course, If you did not look at the charts daily, these fluctuations would mean nothing. If you ony looked at the Australian Index at yearly intervals, 2023 would probably bring some joy. As well as the overall 8% gain for the year, when you include dividends, the ASX 200 Index total return for calendar year 2023 was 12.2%. The ASX “All Ordinaries” Index (Tracking Australia’s largest 500 listed companies) had a total return of 13.0%.

Slack Investor will again emphasize the joy of investing and mostly doing nothing – and trying to focus on longer term returns. One of the best summary charts I have seen for a while that shows calendar year returns has just been updated and published by Ashley Owen. Ashley uses the “All Ordinaries” Index rather than the ASX 200 Index- as there is more historical data available for comparison.

Total ASX “All Ordinaries” calendar year returns – with the the last 5 years highlighted – From Ashley Owen – Owen Analytics – (Click to Enlarge)

The first thing that jumps out in this chart is the amount of “Green” positive years vs the “Red” negative years. In 78% of calendar years, ASX Index returns are positive. The overall average total return since 1900 for the Australian “All Ordinaries” Index is 11.7%.

Inflation has been the topic of the day lately and Owen has kindly provided his calendar year chart in terms of Real Returns for the All Ordinaries Index – The total return minus the inflation rate (Consumer Price Index (CPI)). A certain amount of cash is worth holding to for liquidity – so that you can avoid selling stocks in a market downturn. Although cash can iron out some of the stock market fluctuations, being invested in cash is not a protection from inflation.

Total ASX “All Ordinaries” calendar year “Real” (minus inflation) returns – with the the last 5 years highlighted – From Ashley Owen – Owen Analytics – (Click to Enlarge)

Adjusted for cpi increases, the overall average “Real” total return since 1900 for the Australian “All Ordinaries” Index is 7.9%. Slack Investor is willing to put up with the volatility of share markets for an average “after inflation” return like this.

For financial independence and as a hedge against inflation, it is important to own growth assets – such as the Australian Share market. Sure, there will be the occasional negative annual returns ahead … but let’s not worry about this while the Australian stock market is rising. Long-term overall results are the important thing.

January 2024 – End of Month Update

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

After a big Christmas Rally, things have settled down a bit with modest gains for the ASX 200 (+1.2%) and the S&P 500(+1.6%). The FTSE 100 had a small fall ( -1.3%)

It was time to adjust the stop loss for the S&P 500 as the current value is over 15% greater than the stop loss. Slack Investor has long believed the US market is overvalued and, while enjoying the journey, is happy to have his stop loss a little tighter. It is difficult to do the adjustment on the monthly chart, so I had a look at the weekly chart for the S&P 500 below. I am looking for a dip in the chart that represents a “Higher low”. The new stop loss now stands at 4682 – only 3% below the current value.

{kind=link}